For most users, Zelle feels like magic tap a phone number or email, send money, and it lands in someone’s bank almost instantly. But beyond that simplicity lies a business engine. In this article, we explore how does Zelle make money uncover its revenue streams, and explain how it weaves together banking collaborations, premium services, and industry positioning within digital payment platforms.

We’ll also integrate related terms in a natural way: Zelle business model, Zelle revenue model, Zelle partnerships, peer to peer payments, bank specific policies, merchant services, and more.

What Is Zelle & Why It Stands Out

Zelle is a peer to peer payments network embedded into participating banks’ mobile apps and websites. Rather than having a wallet balance, transactions move money directly from one bank account to another. As of 2023, Zelle processed $806 billion in 2.9 billion transactions, growing 28% year over year.

Because Zelle is native to banking apps, many users never download a separate app. The architecture gives it reach, trust, and the ability to compete directly with third-party apps like Venmo, Cash App, and digital wallets such as Apple Cash.

In this setup, Zelle’s central question is: If users don’t pay fees, how does it make money?

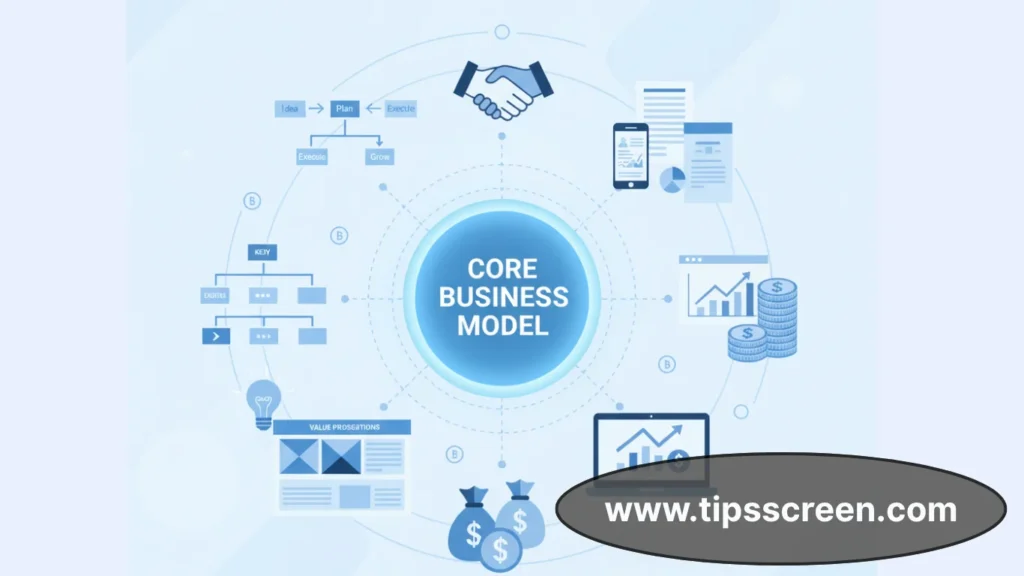

The Core Business Model Explained

At its heart, Zelle’s model is a B2B payment model. Instead of charging users, it earns revenue by collaborating with financial institutions, offering value added services, and enabling features that benefit banks.

Charging Banks, Not Users

Zelle’s primary revenue source is fees or licensing charges paid by partner banks and credit unions. These institutions integrate Zelle technology into their systems, allowing their customers to access instant P2P transfers. Many banks pay for the service based on usage, transaction volume, or feature access.

Because Zelle is co-owned by a banking consortium (via Early Warning Services), the model favors adoption by the banks themselves. Forbes+1

Cost Savings That Benefit Banks

By routing peer-to-peer transfers internally rather than using expensive wire systems or check handling, banks reduce operational overhead. These cost savings for banks effectively subsidize Zelle’s value proposition banks get a way to offer modern payment features while lowering legacy costs.

In many cases, offering Zelle helps a bank retain customers who might otherwise use external fintech apps. In that sense, Zelle contributes to bank customer stickiness, a downstream benefit.

Monetizable Value Added / Business Services

Though the core Zelle for individuals remains free, there are adjacent services with revenue potential:

- Merchant Payments & Point of Sale (POS) Integration: Enabling small businesses to accept Zelle, linked to invoicing or POS systems, so users can pay via bank transfer.

- Invoice Generation & Payment Tools: Tools enabling users or small firms to bill via Zelle.

- Premium Security, Analytics & API Access: Banks may pay extra for advanced fraud detection, analytics dashboards, or API access to integrate with banking infrastructure.

- Cross-Border & International Transaction Services: In future, Zelle could offer cross-border or international payments, which often carry margins higher than domestic transfers.

These features help extend the Zelle revenue model beyond pure transaction fees from banks.

Indirect & Network Effects

Zelle benefits from scale. As usage climbs, the platform becomes more valuable to banks and more difficult for competitors to displace. That scale supports Zelle profitability in the long run.

Also, data can play a role. Aggregated, anonymized trends around payment flow, usage spikes, or risk patterns may help with risk analytics or product development (always with privacy safeguards). Some platforms monetize data insights though Zelle must tread carefully in consumer finance regulation.

How Zelle’s Revenue Streams Fit Together

Let’s break out how the components work in practice.

| Revenue/Value Channel | Description | Role in Model |

|---|---|---|

| Fees from partner banks / licensing | Banks pay to use Zelle’s network, infrastructure, branding | Core B2B income |

| Cost savings for banks | Reduced reliance on legacy transfers, checks | Competitive justification |

| Merchant/Business services | POS integration, invoicing, merchant acceptance | Growth lever |

| Premium/security features | Advanced fraud detection, analytics, API tiers | Upsell path |

| Future cross-border / international | Enabling payments beyond U.S. borders | New high-margin line |

| Network effects / data | Scale benefits, usage-based insights | Long-term strategic value |

When all these align, Zelle achieves profitability without ever charging end users.

Operational Realities & Constraints

To execute its model, Zelle must navigate these practical and regulatory challenges:

Transaction Limits & Bank Policies

Banks set daily and monthly sending limits, often tied to account type, user history, or risk profile. These transaction restrictions serve to mitigate fraud and manage liquidity. Some banks may offer promotional limit increases or adjust limits for long-term customers.

These bank specific policies shape the scale and speed of adoption.

Security, Fraud Checks & Trust

Because transfers are instant and often irreversible, Zelle must maintain robust fraud checks and security methods integration including encryption, real-time threat detection, behavioral monitoring, multi-factor authentication. In 2023, reported fraud remained under 0.1% of transactions, thanks to layered protections.

Still, the platform has faced criticism. A lawsuit by New York’s Attorney General claims that lax protections between 2017–2023 led to over $1 billion in losses. The Verge

Interface & Integration

To maintain seamless adoption, Zelle must ensure that its mobile app interface, embedded features, and digital wallet integration with systems like Apple Cash are smooth and intuitive. Users expect instant transfers with minimal friction.

Competition & Monetization Boundaries

Zelle must carefully balance monetization with user experience. Charging high fees or adding friction could push users back to payment apps that do charge fees but offer rewards, social feeds, or crypto/investment integration (e.g. Cash App, Venmo).

Zelle vs. Other Payment Platforms

Understanding how Zelle positions itself helps clarify why its model works.

Fee Structure & Revenue Approach

- Many peer-to-peer apps charge users or merchants per transaction.

- Zelle, by contrast, leverages bank partnerships and avoids direct user fees.

- It competes by providing a fee free user experience, which helps drive adoption and volume.

Ecosystem Position

- Because Zelle is integrated into banking apps, users often don’t see it as a separate app.

- That integration gives it reach and trust vital in financial services.

- Zelle’s model is closer to digital payment platforms inside financial infrastructure rather than standalone fintech.

Business & Merchant Focus

While platforms like Venmo and Cash App have leaned into social features, investment, and merchant tools, Zelle’s expansion into business oriented services, merchant services revenue model, and POS tools represents its path forward.

As of 2024, more than 7 million small businesses are enrolled in Zelle, and consumer-to-merchant volumes have tripled in recent years.

Growth Metrics & Usage Trends

- Zelle’s 2023 volume was $806 billion across 2.9 billion transactions.

- The network connects over 2,100 banks and credit unions, covering a large share of U.S. deposit accounts.

- Small business usage is rising fast; in 2024, average business payment size was ~$630.

- With growing scale, banks and Zelle can experiment more with premium features or merchant capabilities.

These metrics underscore why Zelle’s model works: volume fuels leverage over partners and infrastructure.

Potential Risks & Challenges

- Scams & Liability: Because funds move instantly, missteps or fraud are hard to reverse. Zelle’s ownership banks have faced lawsuits over fraud losses. AP News+1

- Regulatory scrutiny: As a payment network, compliance (KYC, AML, consumer protection) is heavy.

- International expansion barriers: Currency, legal regimes, foreign rails complex and expensive.

- Competition pressure: Fintechs offering rewards, crypto, or broader financial services may lure away users.

Conclusion

Zelle’s success lies in its clever pairing of user convenience and backend monetization. By making sending and receiving money free for users, it fosters high volume. Behind the scenes, the Zelle business model funnels revenue through bank partnerships, cost-saving incentives, and emerging business services.

So while everyday users might not see a “fee” line on their screen, the earnings come via infrastructure, licensing, and optional features. With growth in Zelle revenue streams, merchant services, and network scale, Zelle is well positioned to remain a backbone of digital payment platforms in the U.S. for years to come.

FAQs: How Does Zelle Make Money?

How does Zelle make money if it doesn’t charge users?

Zelle earns revenue through its partnerships with banks and credit unions. Instead of charging users, Zelle charges partner financial institutions licensing or usage fees. These banks benefit from cost savings, customer retention, and access to modern peer to peer payment features.

What is the Zelle business model?

The Zelle business model is a B2B (business to business) model where revenue comes from banking collaborations and enterprise-level services, not individual users. Zelle integrates directly into bank apps, offering transaction infrastructure, fraud checks, and security methods integration.

Does Zelle charge transaction fees?

Zelle does not charge transaction fees to users for personal transfers. However, partner banks may incur operational costs or fees for offering Zelle’s services. For business oriented services, including invoice generation and POS systems, there may be service-level fees in the future.

Can Zelle be used for international transactions?

Currently, Zelle supports only domestic transfers within the U.S. However, as digital payment platforms evolve, Zelle may explore cross border payment services as a potential future revenue stream. For now, international use is restricted.

Is Zelle safe and secure for money transfers?

Yes, Zelle uses advanced security methods integration to protect transactions. Banks also apply their own fraud checks and may impose transaction restrictions or limits based on customer history. Always verify recipient info before sending money.